Home

You’re currently viewing our content for All Regions.

You can switch to a different region:

May 6, 2025

That all too common look – the scrunched up face, forced smile and slow shake of the head.

Often subconscious but now the default facial expression of the market in response to a simple two-word question… how’s business?

Once the anchor point of small talk, now loaded as the barometer of corporate health.

According to Moxie Research, the results are sobering – 40% of channel partners are still deep in survival mode across Australia.

Many are struggling to overcome lingering economic conditions, notably the cost of doing business crisis that is particularly plaguing homegrown players.

No technology provider is immune to this environment with all organisation types impacted, whether services, consulting, integration or resell.

To call this a soft market would be an understatement however. Thousands of managed service providers (MSP), system integrators (SI) and value-added resellers (VAR) are competing in such a crowded and desperate industry.

Why? Because a tough 2024 has been compounded by a challenging start to 2025.

Anecdotally on this point, channel consensus is clear.

Now, four months into 2025 – and for many, the home stretch of a financial year to forget – this is an ecosystem largely assuming the brace position as the economy continues to twist and turn in uncertain directions.

Moxie Research outlined an unvarnished commentary on the true health of the market aligned to mission-critical financial metrics.

Findings were shared at Moxie Authority 2025, an invite-only conference which housed the most influential figures setting the market agenda in business and technology across Australia.

Aligned to the theme of Inspired Knowledge, this inaugural event in Sydney hosted more than 400 industry front-runners spanning all ends of the ecosystem, from Founders, CEOs and Managing Directors, to CIOs, CTOs, CDOs and CISOs.

Business costs up, competition killers

Even though economic growth in Australia is expected to improve gradually over 2025, based on analyst sentiment, it will remain below trend.

“After a sluggish 2024, Australia’s economy looks as though it may be past the low point for this economic cycle, with the combination of a strong labour market, falling inflation, tax cuts, emerging real wage gains and imminent interest rate cuts contributing to a better-than-expected outlook in 2025,” observed Cathryn Lee, Partner at Deloitte Access Economics.

“However, ‘better-than-expected’ is not the same as ‘good’, as has been revealed by escalating business insolvencies, considerable mortgage stress and a deep per capita recession. Indeed, nobody should get overly excited or complacent. The reality is that the Australian economy remains beset by challenges.”

Notably, the impact of high inflation on the channel should not be underestimated given the substantial increase in operational costs.

Every aspect of running a partner business has become more expensive with salaries considered as one of the most severe, especially for organisations selling ‘people heavy’ offerings such as managed services and consultancy.

This is the context in which partners are making decisions with no organisation immune to this environment.

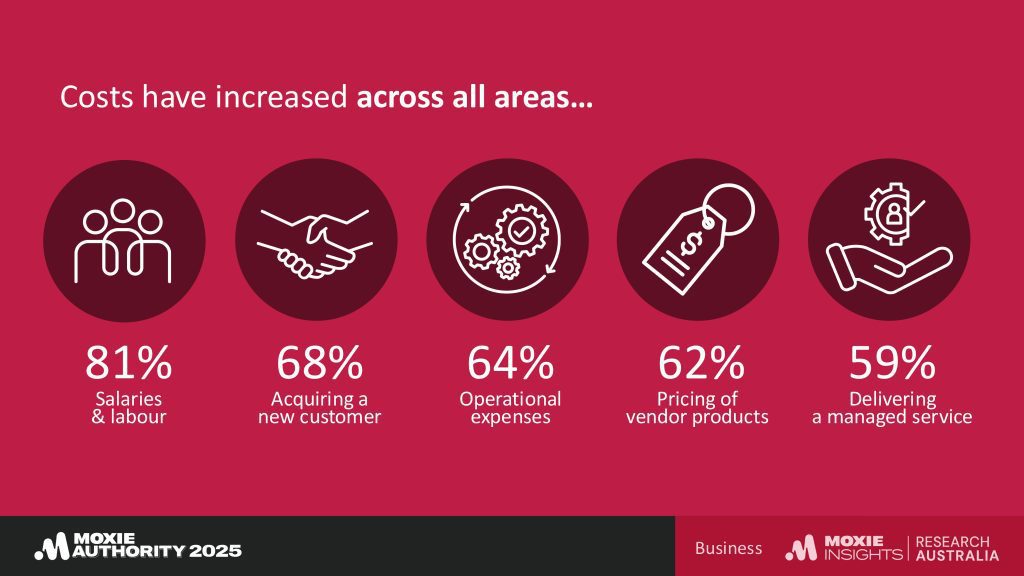

According to Moxie Research, business operating costs have increased for 88% of partners in Australia.

Such a sobering statistic can be directly attributed to the volatile state of the economy during the past 12-18 months.

By way of majority, 41% of partners have experienced a more than 25% increase in the cost of doing business, while almost a third of partners (32%) have suffered an increase of over 50%. Almost a quarter of partners (22%) reported a cost increase of more than 10%.

At the extreme, costs have increased by more than 100% for a small segment of partners (5%).

Based on the data, costs have increased across all areas:

Specific to salaries and labour costs, the channel is feeling the aftershocks of a severe spike in remuneration packages during COVID-19.

During this time, sales and technical talent were enticed by a wave of software-as-a-service (SaaS) vendors committed to paying double – and in some cases, triple – wages to meet inflated demand at the height of the pandemic.

In response, partners have either struggled to retain or acquire talent.

A rebalancing is now underway however given that vendors are laying off thousands of workers locally, regionally and globally – but the damage has been done in that baseline salary expectations have raised significantly across the market.

As many executives shared privately, vendor poaching has now resulted in “average talent commanding eye-watering amounts of money”.

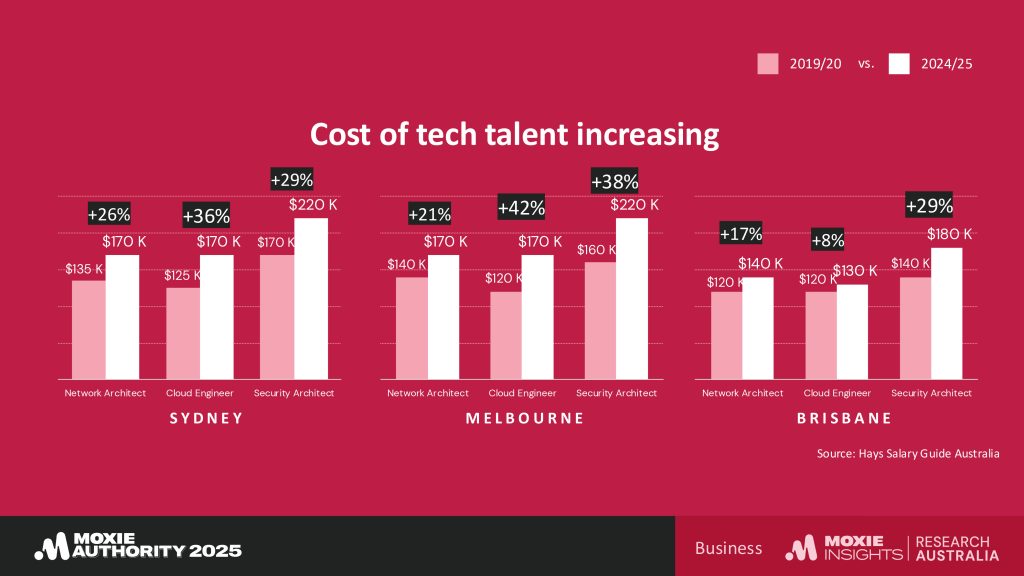

For example, a comparative look at average technical salaries from 2020 to 2025 highlights a double-digit increase almost across the board in Sydney, Melbourne and Brisbane.

The domino effect of increased costs is preventing partner businesses from:

According to Moxie Research, the top five revenue killers for Australian partners are:

The negative impact of a soft market is that vendors – and by extension, partners – are expanding reach and moving into new areas of commercial focus.

Network vendors are moving into cyber security. Cyber security vendors are moving into the network. Enterprise vendors are moving down into the mid-market. SMB vendors are scaling up to the enterprise.

In other words, nobody is staying in their lane.

This is not down to solution expertise or strategic growth strategies however, rather a desperation to go after every available dollar possible.

Vendors have lost patience and are aggressively hunting for new routes to market in response to flat or declining growth. Partners are being dragged along for the ride.

The end result is a feeding frenzy around so many customer accounts – each crammed with battling partners and vendors that on paper, have no right to be there in the first place.

Of course, Australia is no stranger to competition given its ecosystem of approximately 10,000 channel partners. Previously however, market order was shaped by self-assessment by vendors and partners that understood what they did do and perhaps most importantly, what they didn’t do.

Those rules are out of the window in 2025 however – the level of desperation is reaching an all-time high.

Naturally, the intensity of competition is creating a race to the bottom on pricing which is placing enormous strain on partner profitability.

For example, combine the escalating cost of doing business in this economy with vendor product prices increasing, customers wanting to pay less and the channel cutting prices left, right and centre.

The end result is a partner base getting continually squeezed just to stay in the game and be competitive in deals. Throw in the added dimension of vendor marketplaces cutting the partner out entirely in favour of direct customer transactions and this becomes an ecosystem under pressure.

According to Moxie Research, the top five profitability killers for Australian partners are:

Fighting back, room for optimism

Partners remain resilient in the face of tough market conditions however.

To mitigate such uncertainty, some are simply holding the line and preparing for more corporate distress in the months ahead. Yes, pockets of opportunity exist and are being pursued but the headline is that technology providers are proceeding with an abundance of caution.

The most profound decision has been to pass on the additional costs of doing business to customers, as noted by 88% of channel partners in Australia.

According to Moxie Research, the main strategies deployed by executives to tackle rising costs have been centred on:

For many business owners however, the embracing of remote work is more out of financial necessity rather than corporate philosophy.

Post-pandemic, the majority of CEOs privately shared their disappointment that employees didn’t embrace a return to the office at pace. Behind closed doors, questions were asked about the impact to long-term productivity and culture.

As one partner confidentially shared at the time, “I want my team back in the office but I can’t say that because I’d be accused of being a dinosaur.”

Then, a downturn in the economy created a window of opportunity as office leases came up for renewal. Many partners reversed sentiment to downsize or reduce office space to save costs, portraying the decision as based on a commitment to hybrid and remote working.

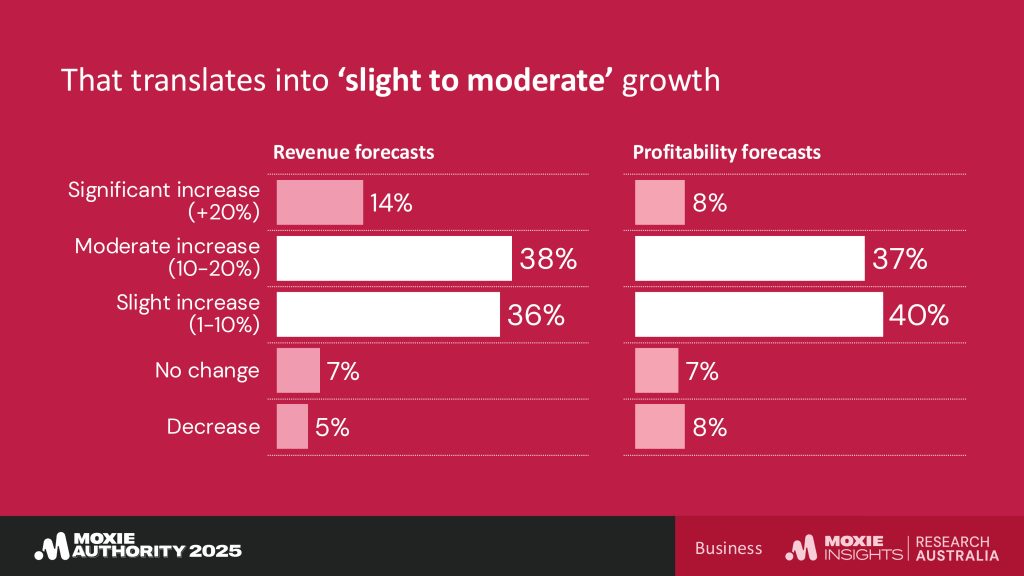

Looking ahead, optimism is returning despite the market downturn.

According to Moxie Research, 76% of partners are expecting growth during the next 12 months, with a further 21% forecasting stability at a minimum. Only 3% remain pessimistic and are preparing for a decline in business.

From a revenue and profitability standpoint, that translates into “slight to moderate” growth based on partner projections for the next 12 months.

In this period of partner pragmatism with appetite for unnecessary risk low, the key word for businesses to define is their interpretation of ‘unnecessary’.

Customer demand will dictate the priorities of partners to an extent but this will be counterbalanced by a constant assessment of ‘nice to have vs. need to have’.

Encouragingly, marketing investment remains in the ‘need to have’ bucket.

This demonstrates that despite additional financial pressures, partners recognise the need to continue acquiring new logos and starting conversations in preparation for the economy stabilising. This is a priority many hope will pay dividends in the medium-term.

In the months ahead, partners will continue this ‘nice to have vs. need to have’ assessment of all business and go-to-market activities. This period of pragmatism will remain until trading conditions improve.

Moxie Authority 2025 housed the most influential figures redefining business and technology across Australia. This inaugural and invite-only conference in Sydney hosted more than 400 industry front-runners spanning all ends of the ecosystem, from CEOs, CIOs and CTOs to CDOs, CISOs and Founders.

Inform your opinion with executive guidance, in-depth analysis and business commentary.