Home

You’re currently viewing our content for All Regions.

You can switch to a different region:

July 3, 2023

Of the 27 leading economists assembled by The Conversation to forecast the financial year that’s just begun, every one expects inflation to continue to fall.

The official quarterly measure of inflation peaked at 7.8% in the year to December and is now 7%, and the newer monthly measure peaked at 8.4% and is now 5.6%.

What’s at issue is how quickly inflation will continue to fall, how many more times the Reserve Bank will push up interest rates to make sure it falls as quickly as it wants, and the damage those rate hikes will do to an already very weak economy.

Twelve of the 27 think a recession is either more likely than not, or an even chance. And almost all expect a “per-capita recession”, in which economic growth fails to keep pace with population growth, sending living standards backwards.

Now in its fifth year, The Conversation survey draws on the expertise of leading forecasters in 25 Australian universities, think tanks and financial institutions – among them economic modellers, former Treasury, International Monetary Fund and Reserve Bank officials, and a former member of the Reserve Bank board.

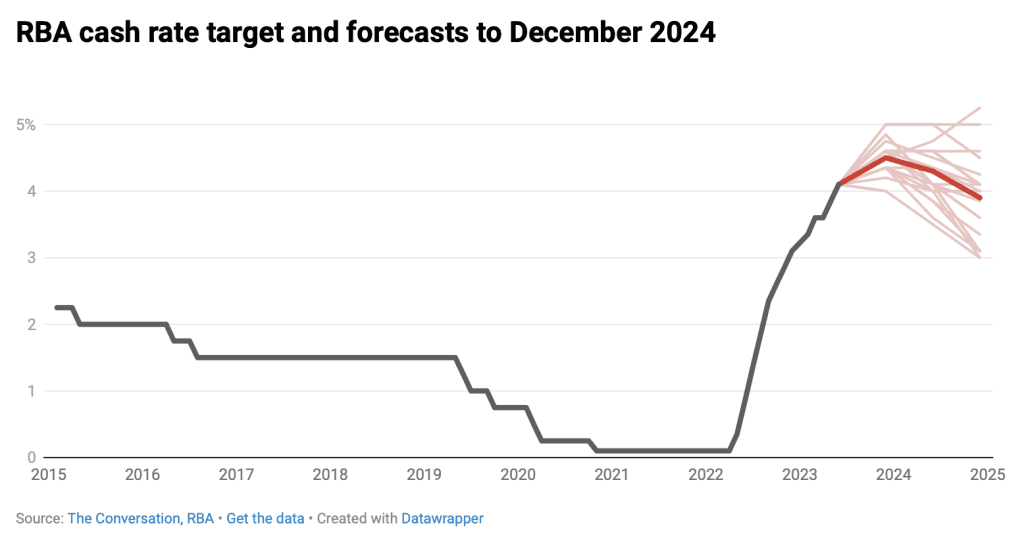

Two more interest rate hikes this year

After 12 interest rate hikes that lifted the Reserve Bank’s cash rate from 0.1% to 4.1% in a little over a year, the panel expects two more.

The panel predicts a cash rate of 4.5% by the end of this year, followed by a decline to 4.3% by the middle of next year, and to 3.9% by the end of 2024.

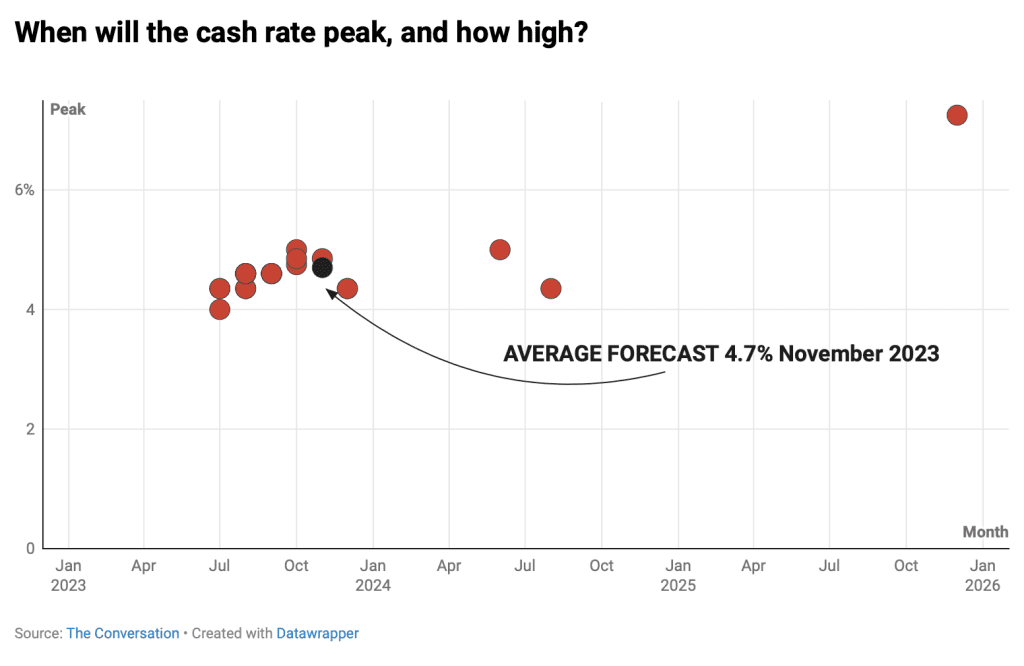

Asked to specify the month in which the cash rate will peak, and how high it will go, the panel settled on a peak of 4.7% in November.

A cash rate of 4.7% would lift the typical rate on a new mortgage from 5.4% to 6%, adding a further $200 per month to the cost of servicing a $600,000 loan.

But the extra pain would be short-lived. Asked how long the cash rate would stay at its peak before being cut, the panel’s average guess was six months, meaning rates would begin to fall in June next year.

Several of those surveyed warned against expecting rates ever to fall back to anything like the emergency lows of 2020 and 2021. Others noted that the one thing that could force the Reserve Bank to cut rates faster than expected was a recession.

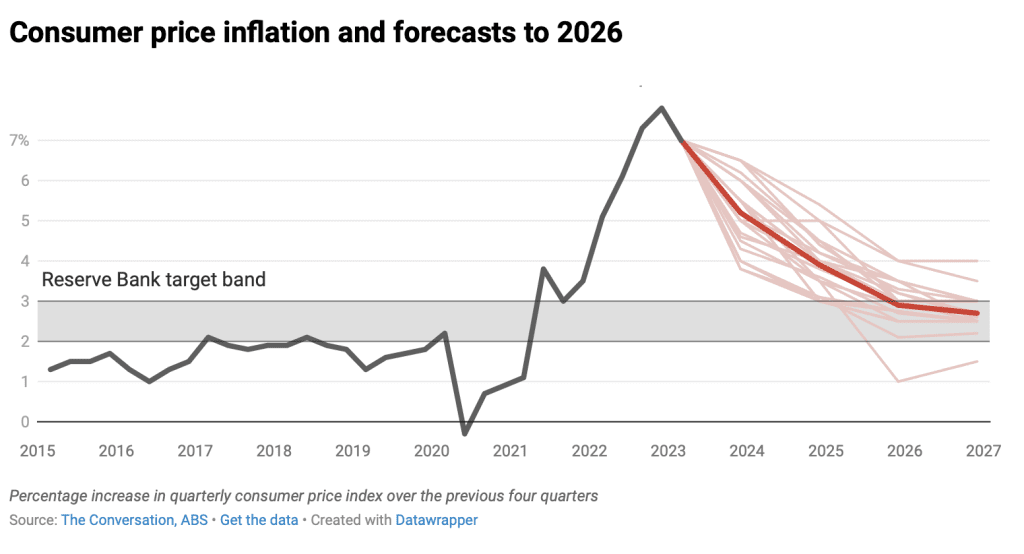

Plummeting inflation, an uptick in real wages

The panel expects inflation to slide from 7% to 5.2% by the end of the year, then to 3.9% by mid-2024, and to 2.9% a year later – putting it back within the Reserve Bank’s 2-3% target band.

Although steep, the fall in inflation isn’t as fast as predicted by the bank itself (3.6% by mid-2024) or the Treasury (3.25% by mid-2024).

Barrenjoey Chief Economist Jo Masters said while price pressure from imported goods and fuel was easing, inflation was increasingly being driven by the prices of services such as rents that tended to be persistent.

Margaret McKenzie of Federation University identified the reopening of borders as a source of downward pressure on prices, saying it would ease labour shortages.

Moody’s Analytics’ Harry Murphy Cruise said although weaker spending was putting downward pressure on inflation, the Reserve Bank seemed unwilling to let that take its course and wanted to slow inflation more quickly, risking “knocking the wind out” of an already fragile economy.

A welcome upside of much lower inflation forecasts is a forecast of the first increase in real wages in three years, albeit a small one.

The panel expects wages growth of 4% in the financial year ahead, just beating price growth of 3.9%. The resulting 0.1% increase in the so-called real wage would be followed by a more substantial increase of 0.7% in 2024-25 as wages growth of 3.6% topped price growth of 2.9%.

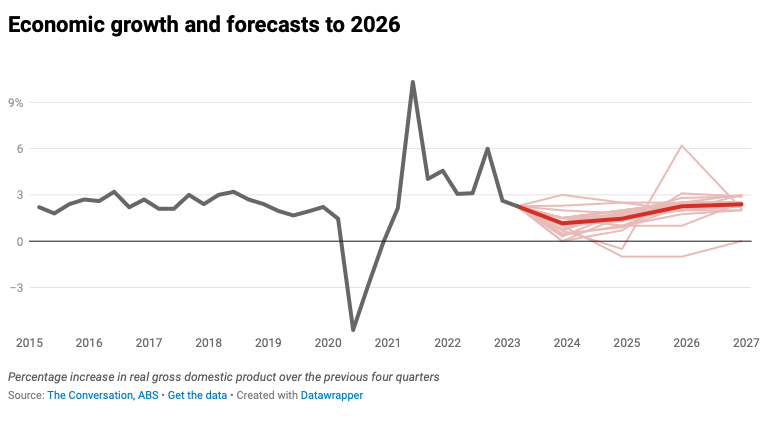

A per-capita (if not an actual) recession

New Zealand is already in a recession, and the panel assigns probabilities of 59% and 42% to the prospect of recessions in the United Kingdom and United States respectively, with the most likely start for both being the final three months of this year.

Throughout 2023, the panel expects economic growth of just 1.2% in the US and historically weak growth of 4.9% in China, suggesting Australia’s biggest customer for minerals will be unable to provide much help as Australia’s own economic growth dwindles.

The panel is forecasting Australian economic growth of just 1.2% in 2023 – the lowest rate outside a recession in more than 30 years, climbing to just 1.5% in the year to June 2024 and 2.3% in the year to June 2025.

AMP Chief Economist Shane Oliver said if the low growth rate turns into what is usually called a recession (two consecutive quarters of shrinking gross domestic product) it will be because the Reserve Bank pushes up interest rates too far for highly indebted Australians to withstand.

He said consumer spending is almost certain to shrink as debt servicing costs hit a record high and, on the Bank’s own analysis, 15% of households with a variable-rate mortgage – roughly a million people – experience negative cash flow.

Asked to estimate the chance of the Australian economy going into recession in the next two years, the panel’s average answer was 38%, well up from the 26% the panel assigned to a recession in February’s survey.

KPMG Chief Economist Brendan Rynne assigned a 100% probability to what he called a “shallow, extended recession”, in which growth is first weighed down by a downturn in housing investment, followed by a slowdown in business investment.

The average forecast start date of a recession, should there be one, is the final three months of this year.

The panel’s economic growth forecast of 1.5% for 2023-24 is well below the Treasury’s forecast of population growth of 2%, suggesting output per person will shrink in what is called a per-capita recession.

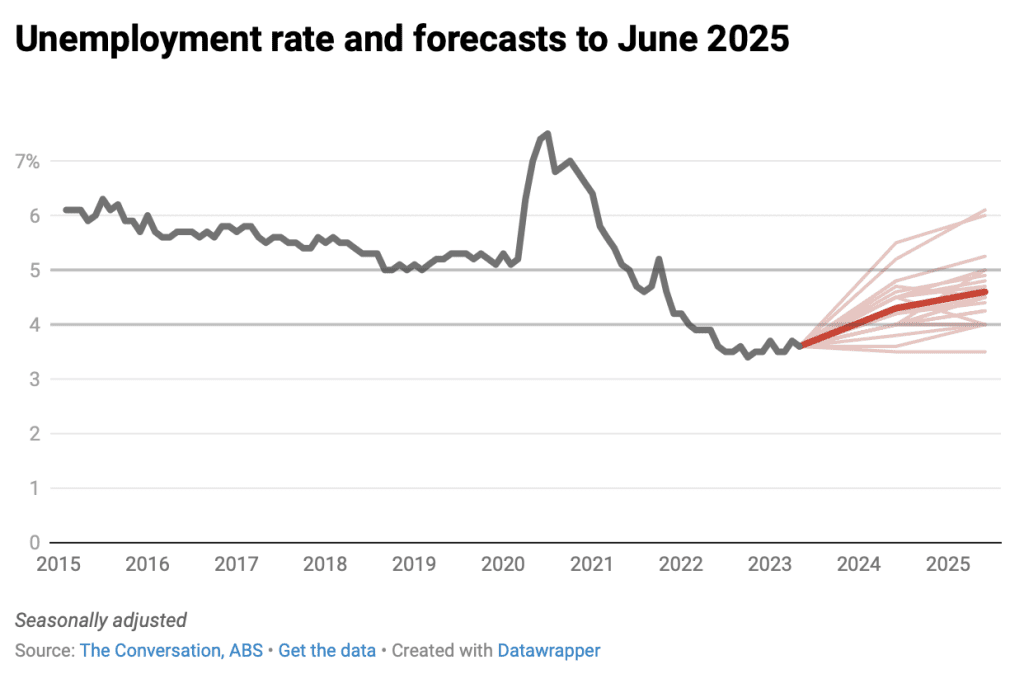

Unemployment climbing, albeit slowly

The panel expects a gradual increase in the unemployment rate from its present near-50-year low of 3.6% to 4.3% by mid-next year, followed by an increase to 4.6% by mid-2025.

The forecasts are in line with those of the Treasury and Reserve Bank, and suggest Australia is unlikely to surrender the big gains in employment made in the aftermath of the COVID lockdowns and return to the pre-COVID unemployment rate of 5%.

University of Tasmania economist Mala Raghavan said while job markets would become less tight as the economy weakened and as foreign students and migrants returned, the impact would be felt first in the underemployment rate, which reflects the extent to which workers are working fewer hours than they want.

Less household buying, higher house prices

The panel expects growth in real household spending of just 1.5% in 2023-24, meaning the amount bought per household is likely to shrink.

Yet at the same time, it is forecasting continued modest growth in home prices, which climbed for the fourth month in a row in June after falling since mid-2022.

Most of the panel expects further growth in Sydney and Melbourne home prices in the 12 months ahead, with only four panel members predicting declines. The average forecast is for both Sydney and Melbourne prices to climb a further 2%.

Former Productivity Commission economist Jenny Gordon identified renewed migration as a driver of demand, offset by declining real wages and the risk of a recession.

Jo Masters said sellers appeared to be withdrawing supply, with total listings a third lower than normal, while the buyers appeared to have higher incomes than before and lower debt-to-income ratios, meaning they were less troubled by high interest rates.

Tiny share market growth, tiny budget deficit

The panel expects the budget surplus for the financial year just ended to be followed by only a tiny budget deficit of A$9.4 billion in 2023-24, which would be less than 0.4% of GDP.

Two panellists, Mariano Kulish and Stephen Anthony, expect this year’s surplus to be followed by another one of $18 billion to 20 billion. Anther, Jenny Gordon, expects this year’s surplus to be followed by a budget in balance.

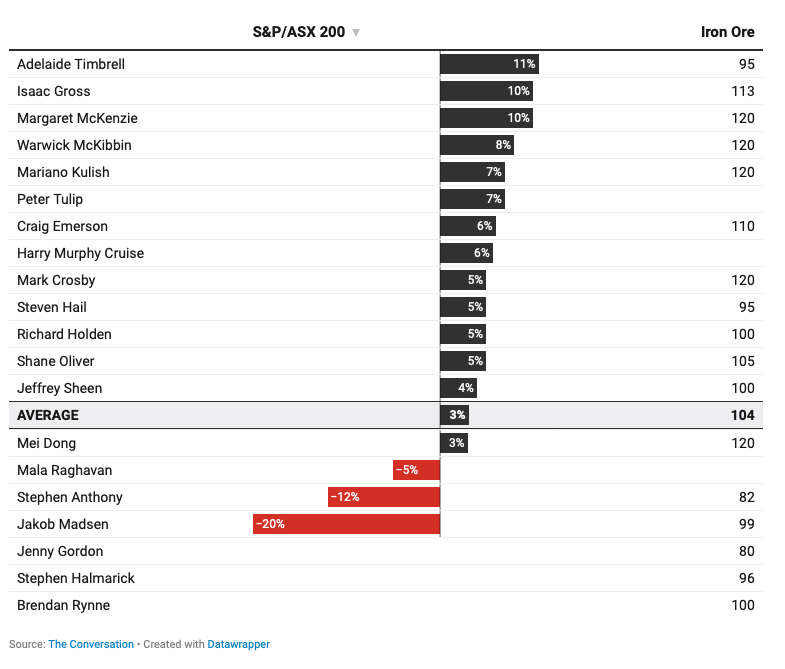

The forecasts reflect an iron ore price expected to stay near US$104 per tonne at the end of the year, instead of falling towards US$60 as forecast in the budget.

The panel expects modest share market growth of 3% in the year to June 2024, with the results sensitive to home prices (through the profits of financial corporations) and minerals prices (through the profits of mining companies).

Peter Martin is Economics Editor of The Conversation and a Visiting Fellow at the Crawford School of Public Policy at the Australian National University. A former Commonwealth Treasury official, he has worked as Economics Correspondent for the ABC and as Economics Editor of The Age. This article was originally published on The Conversation.

Inform your opinion with executive guidance, in-depth analysis and business commentary.