Home

You’re currently viewing our content for All Regions.

You can switch to a different region:

February 19, 2024

Investment in cloud solutions and services reached “new highs” during the final quarter of 2023, with enterprise spending “markedly higher” due to heightened artificial intelligence (AI) enthusiasm.

According to Synergy Research Group estimates, fourth quarter spending on cloud infrastructure services reached $73.7 billion in USD, up by over $12 billion from the same period in 2022. This year-on-year growth rate of 20% was significantly higher than the previous three quarters.

In a further sign of market health, the quarter also grew $5.6 billion from the third quarter in what has been labelled as “by far the largest quarter-on-quarter increase ever achieved”.

For the 12 months as a whole, the market grew 19% with full-year revenues reaching approximately $270 billion.

“While economic, currency and political headwinds have diminished somewhat, it is clear that generative AI technology and services have had a major impact, helping to further boost cloud spending,” observed John Dinsdale, Chief Analyst at Synergy Research.

Findings follow the release of calendar fourth quarter earnings data from most of the major cloud providers, with projections also including infrastructure-as-a-service (IaaS), platform-as-a-service (SaaS) and hosted private cloud services.

As noted by Dinsdale, public IaaS and PaaS services account for the bulk of the market at a growth rate of 21% during the three-month period ending 31 December 2023.

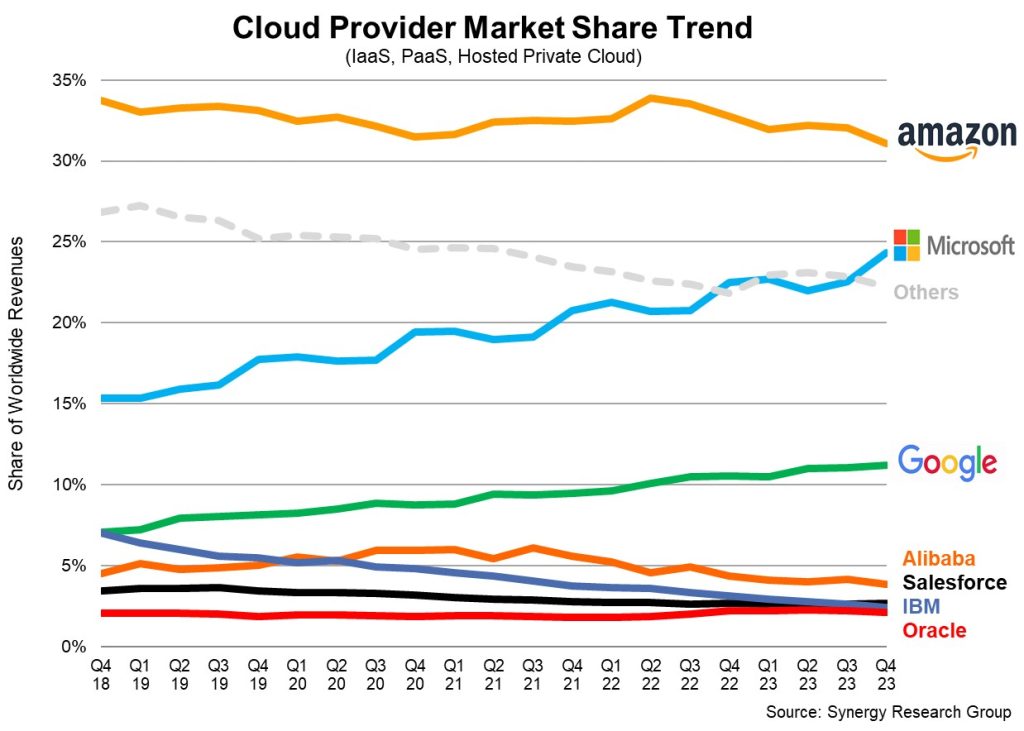

From a competitive vendor standpoint, Google Cloud and Microsoft reported stronger year-on-year growth numbers compared to outright market leader Amazon Web Services (AWS).

Specifically, Microsoft increased its worldwide market share by almost two percentage points to 24% during the fourth quarter while Google Cloud also reported a marginal gain to reach 11%. On the flip side, AWS dropped to 31% in the enterprise despite maintaining strong double-digit growth rates.

“In aggregate the three leaders accounted for 67% of the worldwide market,” Dinsdale added.

Among the tier-2 cloud providers, those with the highest year-on-year growth rates include Huawei, China Telecom, Snowflake, MongoDB, Oracle and VMware.

“The dominance of the major cloud providers is even more pronounced in public cloud, where the top three account for 73% of the market,” Dinsdale said.

Geographically speaking, Synergy reported that the cloud market continues to “grow strongly” in all regions across the world. When measured in local currencies however, Asia Pacific displayed the strongest growth with Australia, Japan, India and China all increasing by 20% or more year-over-year.

“Given improving market conditions and huge excitement around GenAI, Synergy had forecast an uptick in cloud growth rate for the fourth quarter, but the actual growth was even higher than expected,” Dinsdale acknowledged. “Cloud is now a massive market and it takes a lot to move the needle, but AI has done just that.”

Looking ahead, Dinsdale said the law of large numbers means that the cloud market will never return to the growth rates seen prior to 2022.

Despite this, the analyst firm does forecast that growth rates will now stabilise, resulting in “huge ongoing annual increases” in cloud spending. On that basis, Synergy expects the annual cloud market to soon reach the $500 billion mark.

“Helped by AI, there are signs that many enterprises are through their period of belt tightening and of optimising rather than growing their cloud operations,” Dinsdale noted. “AI is helping to open up a wide range of new cloud workloads.”

Inform your opinion with executive guidance, in-depth analysis and business commentary.